New Files Show Epstein Was ‘Too Useful’ for Banks to Drop — Trump Was ‘Too Politically Dangerous’ to Keep

WATCH: New Files Show Epstein Was ‘Too Useful’ for Banks to Drop

The newest Epstein disclosures include deposition testimony that illustrates, in unusually concrete detail, how major financial institutions assessed risk, value, and accountability.

The transcript does not add new allegations about Epstein. Instead, it explains why he remained bankable long after his 2008 conviction and why his relationship with major banks survived despite generating almost no traditional revenue.

That institutional logic is the same logic that later drove JPMorgan to end its ties with Trump Media, and the contrast between the two cases shows how selectively these standards are applied.

In the deposition, Paul Morris—a private banker who handled Epstein’s accounts at JPMorgan Chase and later Deutsche Bank—described Epstein’s financial profile with unusual precision.

Epstein’s trading was minimal. His accounts produced limited fees.

He was not a high-activity client and did not utilize the investment tools that banks rely on to generate consistent revenue. By every conventional benchmark, he was a low-value account.

And yet, the relationship continued.

The deposition shows why. Epstein was not retained for his financial performance but for his institutional usefulness.

Morris acknowledged that Epstein facilitated introductions to ultra-wealthy individuals that the bank viewed as essential prospects. One example was Leon Black, whom Morris identified as a “priority prospect” because of Black’s significant net worth and influence in the investment sector.

Epstein introduced the bank to real-estate investor Andrew Farkas and discussed a potential connection involving biotech investor Boris Nikolic, who had ties to Bill Gates.

These introductions were specific, documented, and initiated by Epstein, not the bank.

This is the key element that many public accounts overlook. Epstein was not being managed as a traditional client. He functioned as a relationship broker inside a system where introductions to power carry more internal value than account-level returns.

Banks routinely emphasize compliance structures, but the testimony shows how those structures contract when the client provides access that cannot be replicated elsewhere.

The selective memory embedded in the transcript reinforces this point. When asked how he learned that Epstein was working with Leon Black, Morris could not recall.

When asked why certain introductions occurred or why Epstein was retained despite low revenue, he could not recall.

Yet he could describe in detail how banks evaluate “priority prospects” and how those prospects affect bonus structures and business development metrics. The difference between what is remembered and what is forgotten reflects the incentives governing the relationship.

That framework becomes even clearer when compared to the treatment of Trump Media & Technology Group.

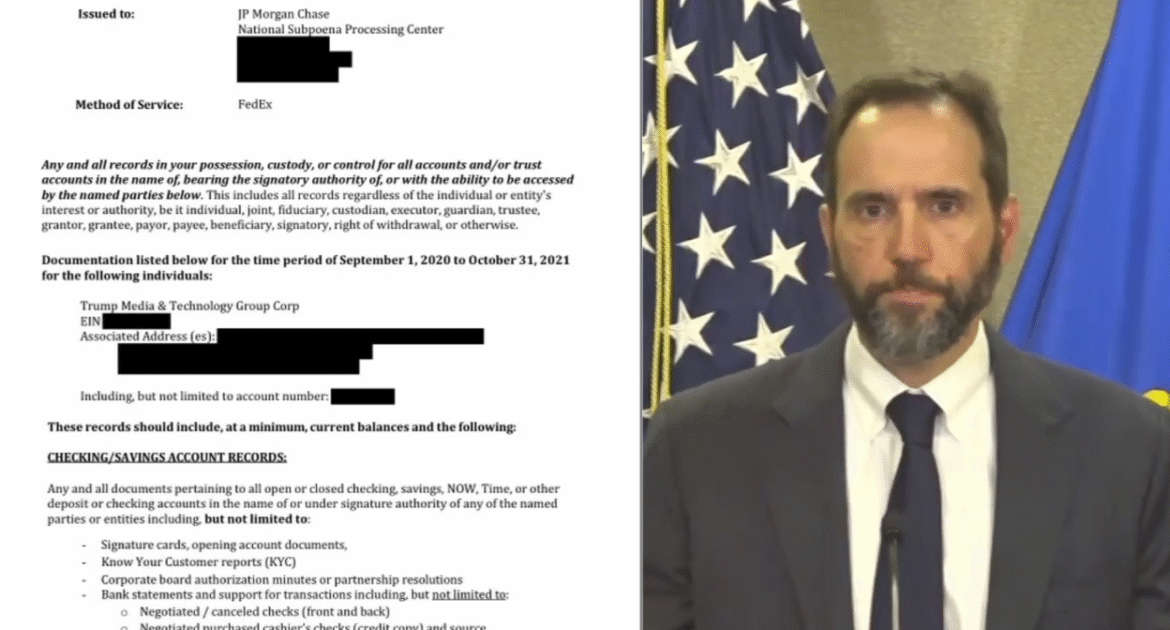

According to public statements from CEO Devin Nunes, Special Counsel Jack Smith secretly subpoenaed JPMorgan for Trump Media’s banking records—even though Trump Media did not exist at the time under investigation.

Trump Media was never notified. Still, JPMorgan complied immediately.

No compliance interpretation justifies executing a subpoena for a non-existent corporate entity.

Banks typically challenge or narrow subpoenas that lack a clear legal nexus. Here, no such step occurred.

The timing worsens the picture. As Trump Media prepared to go public and raise hundreds of millions of dollars, JPMorgan abruptly closed the company’s accounts. The move happened while the DOJ inquiry remained active and at a moment when stable banking relationships were essential to completing the offering.

No new risk factors appeared, and no regulatory action had been taken. The institution acted unilaterally, and its public explanation—that political considerations are irrelevant—is inconsistent with the facts.

Placed alongside the Epstein record, the contrast is direct. Epstein had a criminal record, limited financial activity, and numerous compliance red flags.

The banks retained him because he provided access to high-value individuals. Trump Media had no criminal exposure, no regulatory conflicts, and no financial irregularities. The bank cut it off during a politically charged federal investigation.

Risk was not the differentiating factor. Incentive was.

The new Epstein filing clarifies how major banks navigate these decisions: when a client offers proximity to wealth and influence, the institution absorbs the compliance risk; when a client carries political consequences, the institution distances itself regardless of financial or regulatory standing.

Epstein remained bankable because he was useful. Trump Media became expendable because it was not politically correct, under the Biden DOJ.

The Epstein files reveal a system where access, not ethics, determines who is welcome and who is removed.

The post New Files Show Epstein Was ‘Too Useful’ for Banks to Drop — Trump Was ‘Too Politically Dangerous’ to Keep appeared first on The Gateway Pundit.